Heading

Close X

Menu

If you're thinking about getting a new car, then one of your main concerns will no doubt be how much to budget. Apart from buying a home, purchasing a car is likely the biggest financial commitment most of us will make. Striking the right balance between affordability and getting the vehicle you want requires careful planning.

Here at Wilsons Epsom, "How much should I actually be spending?" is a question we often get asked by customers, so that’s exactly why we’ve created this guide. We're here to help you figure out the numbers that make sense for YOUR budget in 2025. You won’t find any confusing jargon or unrealistic expectations - just straightforward advice to help you drive away happy without your wallet feeling the pinch.

Throughout this guide, we'll explore practical ways to calculate a comfortable car budget, navigate financing options, and help you understand the real costs of ownership. We'll even share some insider tips on getting more car for your money! Read on to find out more…

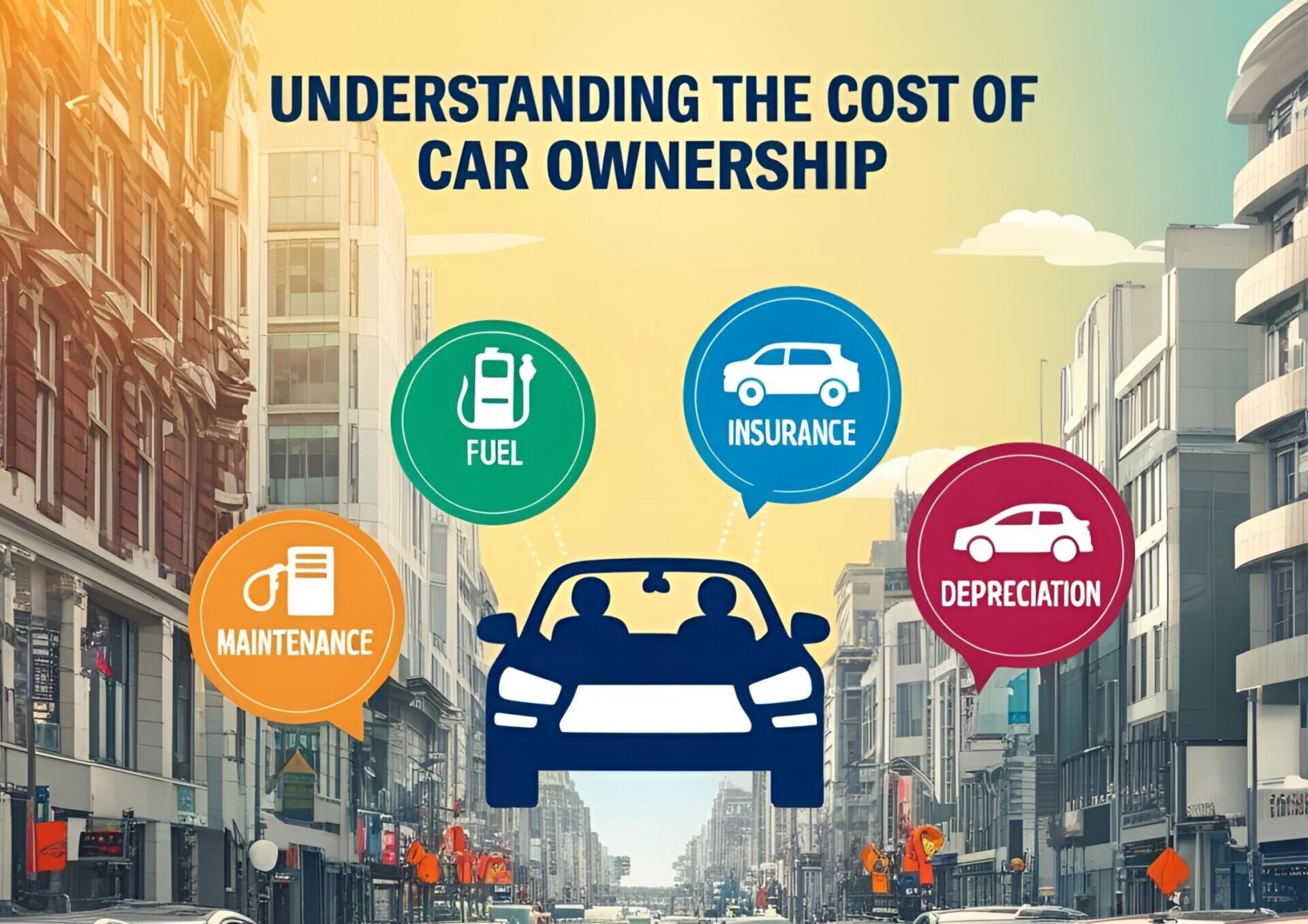

When you’re in the process of setting a budget for a new car, then looking beyond the initial sticker price is absolutely essential. The total cost of vehicle ownership includes several factors that will impact your finances over time:

The purchase price of the vehicle you have your eye on is a natural starting point. No matter whether you're paying cash, taking out a loan, or using a finance plan, how you pay for the vehicle (this may be in part or in full) is just one component of your overall car budget.

If you're not paying for the car upfront from savings, then you'll need to factor in monthly repayment costs and interest payments. Even a small difference in APR (annual percentage rate) can significantly impact your total expenditure over the lifetime of the loan.

Car insurance costs vary dramatically based on the vehicle model, your driving history, and location. Premium vehicles typically cost more to insure, as do cars with higher performance capabilities.

With UK fuel prices consistently among the highest in Europe (eek!), a vehicle's engine efficiency directly impacts your monthly budget. Even a difference of 10 MPG (miles per gallon) can mean hundreds of pounds saved annually on outgoing fuel costs.

It’s important to remember that VED rates vary based on your vehicle's CO2 emissions and list price. In 2025, the rules on road tax in the UK have just changed, meaning that even zero-emission vehicles pay the minimum VED rates, while vehicles with higher emissions can cost over £2,000 to tax in the first year!

Luxury vehicles often come with higher maintenance and repair costs. Because of this, we recommend you budget for regular servicing and unexpected repairs, which increase as the vehicle ages.

Did you know that new cars typically lose 15% to 35% of their value in the first year alone?! This "hidden cost" should influence your budget decisions, especially if you plan to sell the vehicle in a few years time.

If you’ve not heard about the 20/4/10 rule for car budgeting, then allow us to explain more:

For example, if your annual income is £50,000, your car budget should be around £10,000 using this guideline. However, this is just a baseline - your personal circumstances might justify adjusting these figures. Always seek independent advice first.

Another approach to budgeting for a new car is to consider your monthly disposable income after accounting for essentials like housing, utilities, food, and savings. Here's a more detailed breakdown based on income levels:

| Annual Income | Recommended Maximum Budget for Vehicle | Maximum Monthly Payment (for finance) |

| £25,000 | £5,000 - £7,500 | £150 - £200 |

| £40,000 | £8,000 - £12,000 | £250 - £350 |

| £60,000 | £12,000 - £18,000 | £400 - £550 |

| £80,000 | £16,000 - £24,000 | £550 - £750 |

| £100,000+ | £20,000 - £35,000 | £700 - £1,000 |

These figures assume you're following the 20% guideline while also accounting for other vehicle expenses.

Start by reviewing your monthly income and expenses. So you can stay on track throughout the process, be honest about your financial obligations and priorities. Answer these questions:

A larger down payment (this may also be referred to as a deposit or upfront cost) reduces your overall financing costs and monthly payments. It may be that you’ve set savings aside specifically for a vehicle purchase, or made money from trading in your previous vehicle and can put that towards your new purchase.

Aim for a down payment of at least 20% to avoid negative equity and reduce interest payments over the loan term.

Compare finance offers from multiple sources, including manufacturers, dealerships, and brokers, to source the best deal on your new vehicle. Always pay attention to the APR, loan term, and any additional fees or charges. Even a 1% to 2% difference in interest rate can save thousands of pounds over the lifetime of the loan.

Remember that your budget must include all vehicle-related expenses. These will include (but aren’t limited to):

Think about how your financial situation might evolve during your car ownership duration. It’s worth asking yourself the following questions:

One of the most effective ways to stay within budget while getting more car for your money is to consider nearly-new options, such as used/secondhand cars. Vehicles that are between 1 to 3 years old offer several advantages over brand new models:

At Wilsons Epsom, we understand that finding the right vehicle at the right price is essential. Our experienced team is dedicated to helping you find a car that fits both your lifestyle and your budget. We proudly offer extensively checked, high-quality, nearly-new vehicles that deliver exceptional value alongside our new car range.

Whether you're looking for premium luxury, family practicality, or efficient commuting, our diverse range has options to suit every budget. Visit our showroom in Surrey today to explore our extensive range of new and nearly-new vehicles, or contact our finance team to discuss budgeting options tailored to your circumstances.

Setting a realistic budget for your next car purchase involves careful consideration of your financial situation, ongoing costs, and practical needs. By following the guidelines outlined in this article, you'll be well-equipped to make a choice that balances affordability with satisfaction.

Remember that the "right" amount to spend on a car varies significantly between individuals. What matters most is finding a vehicle that meets your needs without compromising your financial wellbeing.

A: Financial experts typically recommend spending no more than 20% of your annual income on a car purchase. For monthly expenses, aim to keep total car-related costs under 10% of your monthly income.

A: Nearly-new vehicles (1 to 3 years old) often prove the best value for money, as they've already experienced significant depreciation while still offering modern features and remaining warranty coverage.

A: While longer terms mean lower monthly payments, they increase your total interest costs. Aim for a 4-year (48-month) financing term for optimal balance between affordable payments and total cost.

A: Leasing typically offers lower monthly payments but no ownership equity. Buying is usually more economical long-term if you plan to keep the vehicle for more than 5 years. Our finance team can help you compare specific options based on your circumstances.

A: Yes! A larger down payment reduces your loan amount, potentially qualifies you for better interest rates, and helps avoid negative equity. Aim for putting down at least 20% of the car’s value when possible.

A: Electric vehicles typically have higher purchase prices but lower running costs (fuel and maintenance). They may also qualify for government incentives and have lower VED rates, making their total cost of ownership competitive despite the higher initial investment.

A: While monthly payments affect your day-to-day budget, focus on the total cost of ownership. A low monthly payment over a very long term can result in paying significantly more overall.

A: Paying cash eliminates interest costs, but consider whether that money might be better invested elsewhere if loan rates are low. Sometimes, financing at a low APR and keeping your cash invested can be financially advantageous.